In the world’s most competitive financial hubs, a statutory audit is far more than a regulatory hurdle; it’s a strategic asset that dictates your global institutional credibility. For international entities, the complexity of Hong Kong Financial Reporting Standards (HKFRS) and the strict 42-day filing window for annual returns often create significant operational friction. You likely recognize that maintaining a clean audit report is essential for securing banking facilities and investor trust, yet aligning these local requirements with global management reporting remains a persistent challenge.

This article provides a comprehensive roadmap to mastering Hong Kong statutory audits and assurance standards to ensure institutional transparency and regulatory compliance. You’ll learn how to navigate the 2025 HKFRS revisions for private entities and leverage expert Hong Kong corporate tax advisory to mitigate non-compliance risks. We explore the mechanics of statutory compliance, the proposed tax reductions for the 2025/26 assessment year, and the strategic steps required to streamline your global entity management with precision and efficiency.

Key Takeaways

- Understand the mandatory requirements of the Hong Kong Companies Ordinance and how the “True and Fair” view reinforces your institution’s financial integrity.

- Distinguish between statutory audits and non-statutory assurance to determine when agreed-upon procedures offer the most efficient route for specific financial verifications.

- Prepare for a frictionless audit by mastering pre-audit planning, materiality thresholds, and the essential documentation required for global reporting standards.

- Evaluate potential partners based on their ability to synchronize audit services with Hong Kong corporate tax advisory for streamlined cross-border operations.

- Implement centralized management strategies that align statutory compliance with long-term growth and investor transparency.

The Statutory Framework of Hong Kong Audit and Assurance Services

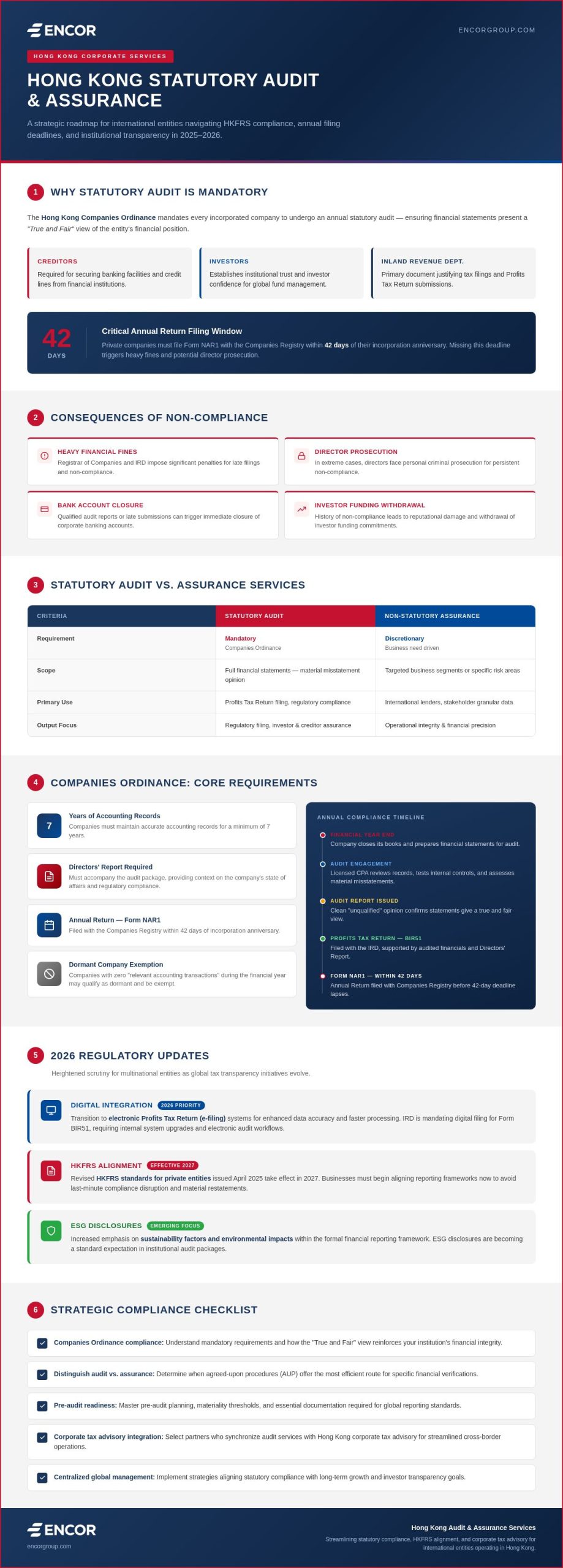

The Hong Kong Companies Ordinance mandates that every company incorporated in the jurisdiction must undergo an annual statutory audit. This isn’t a discretionary exercise but a foundational requirement that ensures financial statements present a “true and fair” view of the entity’s financial position. For global organizations, this audit serves as a critical benchmark for institutional transparency. It provides the high-level assurance required by creditors, investors, and the Inland Revenue Department (IRD). Understanding Hong Kong’s tax system is vital for any entity operating in the region, as the audit report is the primary document used to justify tax filings and financial disclosures.

Failing to meet these statutory obligations carries severe penalties. The Registrar of Companies and the IRD impose heavy fines for late filings, and in extreme cases, directors face personal prosecution. Beyond legal sanctions, the reputational risk is substantial. A qualified audit report or a history of late submissions can lead to the immediate closure of corporate bank accounts or the withdrawal of investor funding. Precision in your Hong Kong corporate tax advisory strategy ensures these deadlines are met with absolute accuracy, protecting your firm’s standing in the international market.

The Companies Ordinance and Financial Transparency

The Companies Ordinance serves as the primary regulatory framework for corporate governance. It requires companies to maintain accurate accounting records for at least seven years. While most entities must submit audited accounts, companies formally registered as dormant are exempt. To qualify as dormant, a company must have no “relevant accounting transactions” during the financial year. Beyond the numbers, the directors’ report must accompany the audit package. This report provides essential context on the company’s state of affairs and its compliance with regulatory standards. Private companies must also file an Annual Return (Form NAR1) with the Companies Registry within 42 days of their incorporation anniversary.

2026 Regulatory Updates in Hong Kong

The 2026 assessment year introduces heightened scrutiny for multinational entities. As global tax transparency initiatives evolve, local audits are becoming more rigorous to align with international standards. The Inland Revenue Department is increasingly moving toward digital filing mandates for the Profits Tax Return (Form BIR51). This transition requires firms to adopt electronic auditing processes to ensure seamless data integration and accuracy. Strategic Hong Kong corporate tax advisory helps businesses prepare for these shifts by aligning internal controls with new digital standards. Key focus areas for the 2026 cycle include:

- Digital Integration: Transitioning to electronic Profits Tax Return (e-filing) systems for enhanced data accuracy and faster processing.

- HKFRS Alignment: Preparing for the 2027 implementation of revised reporting standards for private entities issued in April 2025.

- ESG Disclosures: Increased emphasis on sustainability factors and environmental impacts within the formal financial reporting framework.

Adhering to these updates ensures that your entity remains compliant while benefiting from administrative efficiencies. Proactive planning for these changes prevents the operational bottlenecks often associated with the transition to digital compliance frameworks.

Distinguishing Audit from Assurance: Strategic Implications

While every Hong Kong entity requires a statutory audit, sophisticated global managers recognize the distinct value of non-statutory assurance. A statutory audit provides a high-level opinion on whether financial statements are free from material misstatement, primarily for filing Hong Kong Profits Tax returns. In contrast, assurance services offer targeted insights into specific business segments or risk areas. These reports serve as a trust-building mechanism for international lenders and stakeholders who require granular data beyond a standard audit opinion. They provide a level of comfort that goes beyond mere regulatory compliance, focusing instead on operational integrity and financial precision.

Agreed-upon procedures (AUP) represent a strategic tool within the assurance category. In an AUP engagement, the auditor performs specific tasks defined by the client, such as verifying accounts receivable or auditing royalty payments. Because the auditor doesn’t provide a formal opinion, the resulting report is purely factual, allowing management to draw their own conclusions based on the evidence. This level of detail is often a cornerstone of a robust Hong Kong corporate tax advisory strategy. It allows for precise tax planning and risk mitigation without the overhead of a full-scale audit for every subsidiary or specific financial area. Utilizing these targeted procedures helps global entities maintain a lean yet transparent financial structure.

HKFRS vs. SME-FRS: Choosing the Right Reporting Standard

Selecting the appropriate reporting framework is a critical decision for your entity’s financial architecture. The Small and Medium-sized Entity Financial Reporting Standard (SME-FRS) offers a simplified, cost-effective alternative for companies that meet specific size criteria. To qualify, a company must typically fall below thresholds for annual revenue, total assets, and employee count. For larger or more complex organizations, the full Hong Kong Financial Reporting Standards (HKFRS) are mandatory. For the 2026 assessment year, companies exceeding the qualifying thresholds of HKD 100 million in annual revenue or total assets must transition from SME-FRS to the full HKFRS framework. This transition requires meticulous planning to ensure all historical data aligns with the more rigorous standards.

Assurance Beyond Compliance

In 2026, assurance services are increasingly focused on high-stakes corporate actions. Due diligence assurance is now a standard requirement for cross-border mergers and acquisitions, providing an objective view of a target’s financial health. We also see a significant trend toward Environmental, Social, and Governance (ESG) assurance. International stakeholders now demand verified sustainability data as part of their investment criteria. Coordinating these efforts with international tax advisory services ensures your corporate structure remains tax-efficient while meeting global transparency expectations. If your organization requires a more integrated approach to these complex requirements, exploring comprehensive compliance frameworks can help bridge the gap between local mandates and global standards.

Navigating the Audit Process: A Step-by-Step Reference

A structured audit process transforms a mandatory obligation into a strategic review of your entity’s financial health. Before auditors begin their fieldwork, management must establish a clear framework for scope and materiality. This involves identifying key risk areas, such as significant revenue streams or complex intercompany transactions. By defining these parameters early, you ensure that the audit resources are directed toward the most impactful financial data. This proactive approach is a hallmark of elite Hong Kong corporate tax advisory, where the focus remains on institutional precision rather than mere box-ticking.

Fieldwork involves the auditor testing your data through sampling and third-party confirmations. Expect the audit team to request direct access to bank statements, contracts, and board minutes. This evidence gathering is critical for calculating your final liability under current Profits tax rates. If the data is well-organized, fieldwork typically proceeds without friction, resulting in a cleaner and more efficient review cycle.

The Audit Preparation Phase

Efficiency in the audit cycle depends on the quality of your internal records. You must organize the general ledger and all supporting vouchers, ensuring that every entry is backed by verifiable evidence. Reconciling bank accounts and intercompany balances is non-negotiable; discrepancies here often lead to audit delays and increased scrutiny. For a detailed breakdown of record-keeping standards, refer to the Hong Kong corporate compliance checklist. These standards ensure your entity is prepared for the rigorous testing auditors will perform on your reported income and expenses.

Fieldwork and Reporting Timelines

Clear communication protocols prevent bottlenecks during the query phase. You should designate a single point of contact to handle auditor requests and supplementary evidence. The timeline is tight. Private companies must typically hold their Annual General Meeting (AGM) within six months of the financial year-end. To meet this deadline, the audit must be finalized and signed off well in advance. Integrating your Hong Kong corporate tax advisory into this timeline allows for a seamless transition from the audited accounts to the final tax submission, ensuring you capture all available incentives and reductions.

The process concludes with a review of the draft report and the management letter. The management letter is a valuable document that highlights weaknesses in your internal controls and offers recommendations for improvement. Reviewing these findings allows you to strengthen your operational framework before the next fiscal cycle begins, reinforcing your commitment to global excellence.

Selection Criteria for International Audit and Assurance Partners

Selecting an audit partner for a global entity requires more than a review of technical credentials. A partner must demonstrate mastery of both local Hong Kong standards and the International Financial Reporting Standards (IFRS) that govern global consolidation. This technical depth ensures that local statutory reports align seamlessly with the requirements of an international parent company. Integrating these services with robust Hong Kong corporate tax advisory allows for a unified approach to compliance, where tax planning and audit findings inform one another to optimize the entity’s overall financial position. This synergy prevents the fragmented reporting that often leads to regulatory scrutiny or missed tax incentives.

Beyond technical standards, sector-relevant experience is a primary differentiator. An audit firm with specific insights into your industry, whether in high-growth technology, global logistics, or financial services, can identify risks and opportunities that a generalist might overlook. This expertise translates into more meaningful management letters and strategic recommendations that add value beyond the audit opinion. A partner who understands the nuances of your sector can anticipate the specific challenges your finance team will face during the annual review cycle.

Assessing Global Reach and Local Depth

A partner must possess deep roots in the local regulatory environment while maintaining a sophisticated grasp of international markets. This dual focus is essential for organizations executing a global business expansion strategy. Evaluating the firm’s standing with the Accounting and Financial Reporting Council (AFRC) provides an objective measure of their reliability. A firm that is respected locally and understands global complexities ensures your entity remains a low-risk, high-transparency operation in the eyes of both the government and international stakeholders.

The Role of Technology in Modern Auditing

Digital transformation has shifted the audit process from manual sampling to comprehensive data analytics. Leading partners utilize cloud-based platforms for secure data exchange, ensuring that sensitive financial information remains protected throughout the engagement. AI-driven anomaly detection now allows auditors to scan entire datasets for irregularities, providing a level of precision that traditional methods cannot match. Modern audit software automates routine data validation, which significantly reduces the administrative burden on the client’s internal finance team. This shift toward automation allows your staff to focus on strategic growth rather than manual document retrieval.

Responsiveness remains the final, critical criterion. For global headquarters operating across multiple time zones, a partner who prioritizes clear and timely communication is indispensable. If you are seeking a partner who combines these technical and technological advantages with proactive support, you can consult with our compliance experts to align your Hong Kong operations with your global objectives.

Integrating Audit into Global Entity Management with Encor Group

Encor Group streamlines the critical intersection of statutory requirements and operational efficiency. By positioning the annual audit as a core component of a broader management strategy, we eliminate the silos that often lead to data discrepancies and missed deadlines. Our expertise in Hong Kong corporate tax advisory ensures that your audit findings are immediately translated into tax-efficient actions, protecting your bottom line while maintaining institutional transparency. This integrated approach allows global headquarters to maintain a clear, real-time view of their Hong Kong subsidiary’s standing without getting bogged down in local administrative nuances.

The synergy between our Hong Kong company formation services and ongoing compliance management provides a seamless lifecycle for your entity. From the initial incorporation to the finalization of audited accounts, we ensure that every corporate secretarial filing and accounting entry supports your long-term objectives. Managing international payroll solutions alongside these reports further consolidates your global data, reducing the risk of non-compliance in labor and tax regulations. We act as the primary bridge between local auditors and your global finance team, ensuring that technical queries are resolved with precision and speed.

Centralized Compliance for Multinationals

Encor Group reduces operational friction by integrating bookkeeping with direct audit coordination. We maintain consistency across multiple markets through a single platform that allows global teams to access necessary documentation instantly. Our proactive management of Hong Kong company secretary requirements ensures your entity never misses a filing deadline. This centralized model provides a unified source of truth for your financial data, which is essential for maintaining a clean audit trail and facilitating smooth communication with international stakeholders.

Strategic Advisory for Long-Term Growth

We use audit insights as a diagnostic tool to optimize your global operations. Instead of viewing the audit as a historical record, we treat it as a strategic reference that identifies areas for cost reduction and operational scaling. This preparation is vital for entities planning future capital raises or market expansions. By aligning your local compliance with global standards, we ensure your organization is always prepared for high-level due diligence. You can contact Encor Group today for a strategic consultation to align your Hong Kong corporate tax advisory needs with your global growth ambitions.

Securing Global Institutional Credibility through Strategic Compliance

Mastering the Hong Kong statutory framework is a prerequisite for any global entity seeking to maintain a stable and transparent international presence. By distinguishing between mandatory audits and strategic assurance, your organization can move beyond mere compliance to achieve operational excellence. It’s essential to recognize that efficient document preparation and the selection of a technologically advanced partner are the primary drivers of a frictionless reporting cycle.

Integrating these requirements with expert Hong Kong corporate tax advisory ensures that your financial disclosures reinforce your broader commercial objectives. Encor Group offers comprehensive tax, accounting, and compliance advisory services with a specific focus on multinational entity management. With an established global presence in 10+ markets, we facilitate the seamless coordination of your local requirements with your global headquarters’ reporting standards.

Consult with Encor Group for Strategic Hong Kong Audit Coordination to transform your regulatory obligations into a pillar of institutional strength. We’re ready to help you navigate these complexities with precision and confidence.

Frequently Asked Questions

Is a statutory audit mandatory for all Hong Kong companies in 2026?

Yes, a statutory audit remains mandatory for all companies incorporated in Hong Kong for the 2026 assessment year. The only general exemption applies to companies that have formally applied for and received dormant status from the Companies Registry. Every other entity must appoint a Hong Kong Certified Public Accountant to verify that their financial statements provide a true and fair view of their fiscal position. This ensures transparency and maintains the integrity of the local financial system.

What is the difference between an audit and a review engagement in Hong Kong?

An audit provides reasonable assurance that financial statements are free from material misstatement, while a review engagement offers only limited assurance. Statutory requirements in Hong Kong specifically demand a full audit to satisfy the Inland Revenue Department’s filing mandates. Review engagements are typically utilized for internal management purposes or specific stakeholder requests; however, they don’t fulfill the legal obligations established under the Companies Ordinance for annual reporting.

How long must a Hong Kong company keep its financial records for audit purposes?

Hong Kong companies are legally required to maintain their accounting and financial records for a minimum of seven years. This retention period ensures that the entity can provide sufficient evidence for any retrospective audits or tax investigations. Records must include all vouchers, bank statements, and contracts that substantiate the transactions recorded in the general ledger. Failing to maintain these records can result in significant fines and legal complications for the company directors.

Can a Hong Kong company use international accounting standards (IFRS) instead of HKFRS?

While HKFRS is closely aligned with IFRS, it’s common for Hong Kong incorporated companies to adopt the local standards for their statutory filings to ensure full compliance. Certain multinational entities might prepare financial statements under IFRS for global consolidation, but they must ensure these reports also comply with local statutory requirements for their Hong Kong filings. Professional Hong Kong corporate tax advisory helps determine the most efficient reporting framework for entities with complex cross-border operations.

What are the penalties for late filing of audited financial statements in Hong Kong?

Late filing of audited financial statements triggers escalating fines from the Companies Registry and potential prosecution of the company’s directors. The Inland Revenue Department also imposes surcharges and penalties for the late submission of the Profits Tax Return, which must include the audit report. Consistent non-compliance can lead to the disqualification of directors and severe reputational damage within the international banking community, often resulting in the immediate closure of corporate accounts.

How much does a typical Hong Kong audit service cost for an SME?

The cost of a statutory audit in Hong Kong varies significantly based on the company’s transaction volume, the complexity of its operations, and the quality of its internal record-keeping. SMEs with straightforward financial structures typically face lower fees than multinational entities with diverse revenue streams. Because every engagement is unique, you should seek a tailored proposal that reflects your specific operational requirements rather than relying on generalized industry estimates that don’t account for your specific risk profile.

Can a dormant company be exempt from audit requirements in Hong Kong?

A company can be exempt from audit requirements only if it is formally registered as a “dormant company” with the Hong Kong Companies Registry. To maintain this status, the entity must have no relevant accounting transactions during the financial year. If a company resumes operations or enters into any transaction that requires an accounting entry, it loses its dormant status and must immediately fulfill all statutory audit and filing obligations as required by the Companies Ordinance.

What documents are required to prepare for a Hong Kong statutory audit?

Preparing for an audit requires a comprehensive set of documents, including the trial balance, general ledger, and all bank reconciliation statements. You must also provide supporting evidence such as sales invoices, purchase receipts, and executed contracts. Auditors will review board minutes and director declarations to ensure corporate governance standards are met. Utilizing a robust Hong Kong corporate tax advisory partner ensures that your documentation is organized and ready for the rigorous review process so you don’t face unnecessary delays.