For the modern enterprise, an offshore bank account isn’t a luxury; it’s a strategic pillar of operational excellence. While the global financial environment of 2026 demands absolute transparency through FATCA and the OECD’s Pillar Two framework, the primary challenge for executives remains the friction of rigorous KYC and AML requirements. You likely find that opening offshore banking accounts for non-resident entities is increasingly complex, often leading to concerns regarding compliance with evolving international tax reporting standards.

This article provides an authoritative overview of how these accounts serve as a foundation for capital mobility and institutional stability. We’ll examine the process of selecting reputable jurisdictions and aligning your banking relationships with your corporate structure to ensure seamless multi-currency management. By the end of this guide, you’ll understand how to secure the financial infrastructure necessary for global trade while maintaining the highest standards of regulatory compliance.

Key Takeaways

- Establish a foundation for international operational excellence by understanding the strategic role of offshore banking accounts in modern corporate structures.

- Optimize multi-currency management and capital mobility to mitigate foreign exchange risks and facilitate seamless global trade.

- Navigate the rigorous landscape of international KYC and AML protocols to ensure long-term institutional stability and regulatory compliance.

- Evaluate strategic jurisdictions based on political stability, regulatory reputation, and alignment with your specific corporate finance requirements.

- Streamline the account opening process through expert advisory that integrates financial setup with entity incorporation for maximum efficiency.

Defining Offshore Banking Accounts for the Global Enterprise

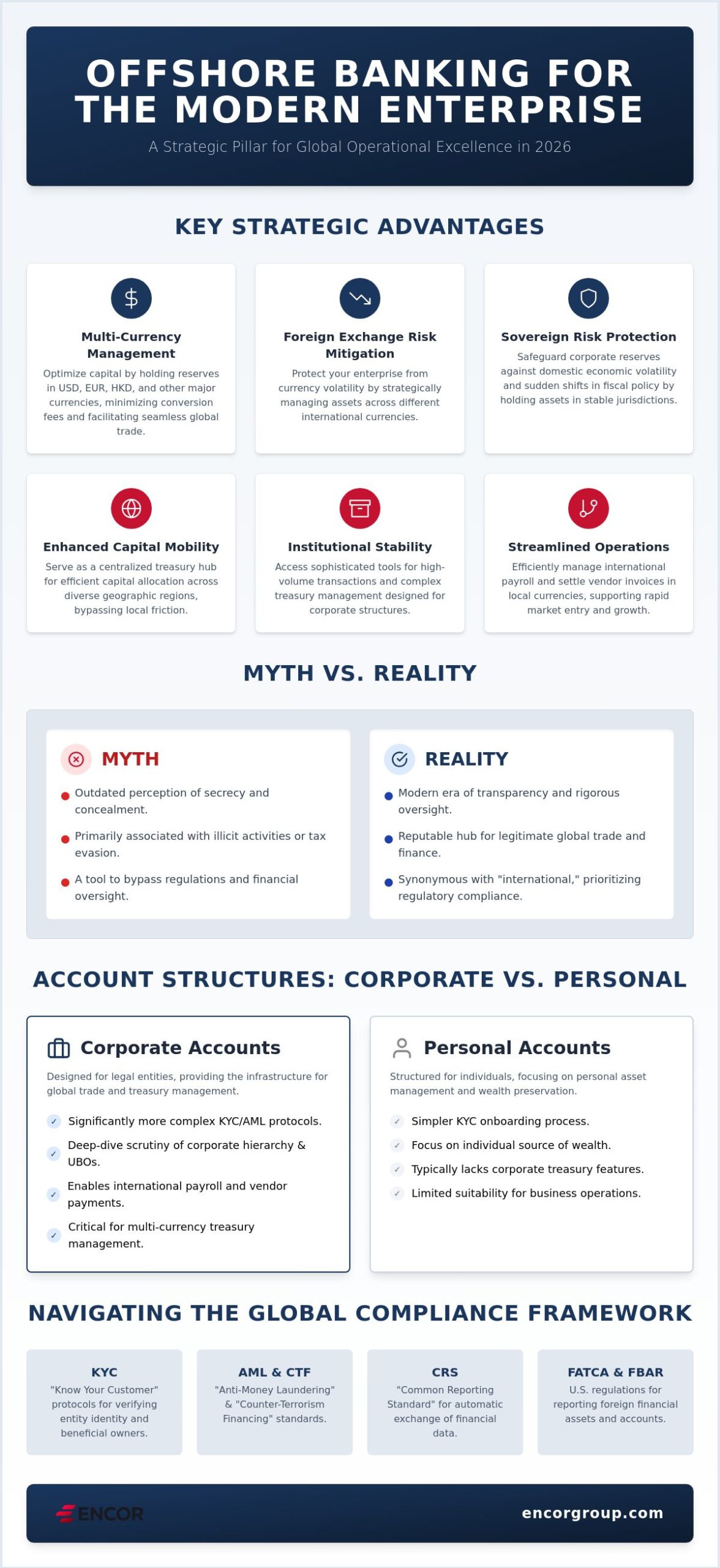

An offshore banking account is a financial facility maintained in a jurisdiction separate from a company’s primary place of registration or operational headquarters. In the context of 2026 global finance, these accounts serve as sophisticated tools for institutional stability and capital mobility. They provide businesses with access to international capital markets and diverse currency options that domestic institutions often cannot match. Unlike traditional retail banking, which focuses on localized consumer services, institutional offshore facilities are designed for high-volume corporate transactions and complex treasury management.

The industry has undergone a fundamental transformation. It has moved from a legacy of secrecy to a modern era of transparency and rigorous oversight. An Offshore bank today operates within a framework of international standards, functioning as a reputable hub for legitimate global trade. This evolution ensures that offshore banking accounts are recognized as essential components of a robust corporate financial structure rather than tools for concealment.

Corporate vs. Personal Offshore Accounts

Structuring an account for a legal entity involves significantly more complex KYC (Know Your Customer) protocols than those required for individuals. Banks conduct deep-dive scrutiny of the entire corporate hierarchy, including ultimate beneficial owners and the specific source of corporate wealth. While the onboarding process is more intensive, the operational advantages for businesses are substantial. Legal entities can manage international payroll and settle vendor invoices in multiple local currencies, which effectively eliminates many foreign exchange conversion fees. This financial infrastructure is a critical component of a successful global business expansion strategy. It provides the necessary liquidity and regional presence to support rapid market entry and sustained growth.

Common Myths vs. Institutional Realities

Outdated perceptions often link international banking with illicit activities. Modern AML (Anti-Money Laundering) and CTF (Counter-Terrorism Financing) standards have largely dismantled these associations for reputable institutions. Under the Common Reporting Standard (CRS), financial data is shared automatically between participating nations to ensure total tax transparency. In 2026, the term “offshore” is effectively synonymous with “international.” It describes a strategic approach to asset management that prioritizes institutional stability and regulatory compliance. Businesses that utilize these accounts don’t seek to bypass regulations; they seek the professional efficiency and risk mitigation that global financial centers provide.

Strategic Advantages of Maintaining International Banking Facilities

Maintaining international banking facilities provides a sophisticated framework for managing global liquidity and operational risk. For multinational enterprises, these accounts function as a centralized treasury hub, allowing for the efficient allocation of capital across diverse geographic regions. This institutional centralization is particularly beneficial for entities operating in high-growth markets like Asia or the Middle East, where local banking infrastructure might present bureaucratic hurdles. By utilizing offshore banking accounts, corporations can bypass regional friction and maintain a consistent standard of financial management.

One primary advantage involves protection against sovereign risk and domestic economic volatility. In 2026, global markets remain susceptible to sudden shifts in fiscal policy or local currency devaluation. Holding assets in a reputable international jurisdiction provides a necessary buffer. It ensures that corporate reserves remain accessible and stable regardless of local conditions. Businesses with U.S. reporting obligations must remain cognizant of compliance requirements, such as the Report of Foreign Bank and Financial Accounts (FBAR), which applies if the aggregate value of foreign accounts exceeds $10,000 at any time during the calendar year.

Multi-Currency Management and FX Risk Mitigation

Effective multi-currency management is essential for mitigating foreign exchange (FX) risk. Corporations often hold reserves in major currencies like USD, EUR, HKD, or AED to match their specific operational liabilities. This strategy eliminates the need for frequent and costly currency conversions. It also lowers transaction costs for cross-border trade and facilitates seamless international payroll solutions. Within these offshore platforms, businesses can utilize advanced financial instruments like spot and forward contracts to lock in exchange rates and protect their profit margins against market fluctuations.

Capital Mobility and Global Market Access

Institutional offshore facilities provide unparalleled capital mobility. They allow for the rapid deployment of funds for international acquisitions or strategic investments. Unlike domestic banks, these institutions often offer specialized credit facilities and trade finance instruments tailored for global operations. This access is vital for high-net-worth individuals and family offices that require sophisticated investment products not typically available in retail markets. If you’re looking to optimize your corporate structure, our team can provide bank account opening assistance to ensure your financial setup matches your global ambitions.

Navigating the Regulatory Framework: Compliance and KYC Standards

The regulatory environment for international finance has transformed into a high-transparency ecosystem. Banks now function as front-line regulators, enforcing stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols. Corporate applicants must provide exhaustive documentation regarding their business model, expected transaction volumes, and the origin of capital. These measures aren’t merely bureaucratic. They’re legal requirements designed to combat Counter-Terrorism Financing (CTF) and ensure the integrity of the global financial system. When opening offshore banking accounts, you must expect a level of scrutiny that matches the complexity of your international operations.

Modern jurisdictions, including the British Virgin Islands and Seychelles, now enforce “Economic Substance” laws. Banks frequently verify that an entity has a genuine presence and conducts management activities within its registered jurisdiction. This shift prevents the use of “shell” companies and ensures that the financial activity aligns with the legal structure. Businesses must also remain vigilant regarding U.S. reporting requirements for foreign accounts. For instance, the FBAR mandates disclosure for accounts exceeding an aggregate value of $10,000 at any point during the calendar year. Compliance with the Foreign Account Tax Compliance Act (FATCA) also remains a critical priority for entities with U.S. connections.

Understanding Beneficial Ownership and Transparency

Transparency is the cornerstone of the 2026 banking environment. Institutions require full disclosure of Ultimate Beneficial Owners (UBOs), which generally includes individuals holding significant control or equity. A transparent corporate hierarchy simplifies the onboarding process. Banks utilize centralized registers of beneficial ownership to verify information and assess risk. Any opacity in the ownership chain often results in immediate application rejection. It’s essential to present a clear, documented path from the entity to the individual owners to satisfy institutional due diligence requirements.

The Role of AEOI and CRS in Modern Banking

The Automatic Exchange of Information (AEOI) framework, governed by the Common Reporting Standard (CRS), ensures that tax authorities share financial data across borders automatically. This system makes it vital for companies to clearly establish and document their tax residency. Compliance isn’t a one-time event. It involves ongoing account reviews and periodic updates of corporate records to reflect any changes in the business structure. Maintaining accurate documentation is essential to avoid account freezes or the termination of the banking relationship. Banks prioritize clients who demonstrate a proactive commitment to these international reporting standards.

Jurisdiction Selection: Strategic Hubs for Corporate Finance

Selecting a strategic jurisdiction for your corporate capital involves a calculated evaluation of regulatory reputation and institutional stability. Executives must prioritize jurisdictions that avoid the FATF grey list. This prevents the transaction delays and increased scrutiny often associated with deficient anti-money laundering regimes. A jurisdiction’s legal system provides the necessary predictability for contract enforcement. For instance, the Common Law foundation in Hong Kong offers a familiar and robust framework for international dispute resolution, making it a primary choice for offshore banking accounts.

Operational logistics also dictate the selection process. Time zone alignment ensures that your treasury team can communicate with bank officers during standard business hours without delay. Language support is equally vital; banks that provide documentation and advisory in your primary business language reduce the risk of administrative errors. You should evaluate minimum deposit requirements and ongoing maintenance fees, as these vary significantly between established tier-one hubs and emerging markets. A methodical approach to selection ensures that your financial infrastructure aligns with your long-term operational goals.

Hong Kong as a Gateway to Asia-Pacific

Hong Kong remains a premier destination due to its world-class regulatory environment and the total absence of exchange controls. It serves as an essential conduit for entities trading with Mainland China, offering specialized banking products for cross-border commerce. Utilizing Hong Kong company formation services allows businesses to integrate into this ecosystem while benefiting from a territorial tax regime. Under current 2026 regulations, qualifying entities can benefit from a 0% tax rate on foreign-sourced profits, provided they meet the necessary compliance standards.

The UAE and the Rise of Middle Eastern Financial Hubs

Dubai and Abu Dhabi have emerged as neutral, high-growth financial centers that bridge the gap between Eastern and Western markets. UAE Free Zones offer distinct advantages, including 0% corporate tax for qualified businesses and the full repatriation of capital and profits. Non-resident entities can access these hubs, provided they demonstrate genuine economic substance and meet the rigorous KYC requirements of the Emirates. The banking landscape here is characterized by modern digital interfaces, making it a preferred choice for managing offshore banking accounts in the Middle East. To secure your position in these strategic hubs, you can utilize our professional bank account opening assistance to streamline the application process.

Facilitating Institutional Bank Account Opening with Encor Group

Securing a robust financial foundation requires more than a simple application; it demands a strategic alignment between your corporate structure and the bank’s specific risk appetite. At Encor Group, we recognize that the most frequent cause of application rejection is a lack of comprehensive preparation or a failure to articulate the business model to bank underwriters. Our advisory services bridge this gap by ensuring that your entity presents a low-risk profile from the outset. By the time we submit your file, every regulatory requirement is addressed, which significantly increases the probability of a successful outcome for your offshore banking accounts.

The contemporary financial landscape of 2026 dictates a proactive approach. It’s now a recommended industry standard to secure a banking relationship before finalizing the formation of an offshore company. This prevents the costly mistake of incorporating an entity that remains unable to access international payment rails. We facilitate this synergy by integrating our bank account opening assistance with our core incorporation services. This methodical progression ensures that your financial setup is not an afterthought but a central pillar of your global operational strategy.

Strategic Advisory and Documentation Support

A successful application relies on the quality of the business profile presented to the institution. Our team assists in drafting a comprehensive narrative that details your flow of funds, primary counterparties, and anticipated transaction volumes. We also manage the intensive administrative requirements, such as the certification of corporate documents through apostille or legalization processes. By coordinating directly with bank officers, we streamline the KYC process and handle requests for additional information with institutional precision. This high-level coordination reduces the administrative burden on your executive team and accelerates the onboarding timeline.

Integrating Banking with Global Entity Management

Institutional stability is maintained through ongoing compliance and meticulous record-keeping. Once your account is active, our corporate secretarial services ensure that your entity remains in good standing, which is vital for maintaining uninterrupted banking access. We align your banking facilities with your broader accounting and tax advisory needs to create a seamless financial ecosystem. This integrated approach ensures that every regulatory filing and periodic account review is handled with the same rigor as the initial application. To begin building a secure and scalable financial infrastructure, you can engage our specialists for comprehensive bank account opening assistance and regulatory advisory.

Securing Your Global Financial Infrastructure

Establishing robust offshore banking accounts is a fundamental requirement for any enterprise seeking international operational excellence. Success in this environment depends on a methodical approach to jurisdiction selection and an unwavering commitment to institutional transparency. By aligning your corporate structure with the specific requirements of premier hubs like Hong Kong or the UAE, you ensure both capital mobility and long-term stability. The 2026 financial landscape demands a level of precision that only a seasoned advisor can provide.

Encor Group operates as a strategic navigator across more than 10 global markets. We specialize in handling the complexities of high-stakes KYC and regulatory compliance to ensure your applications meet institutional standards. Our established presence in key financial centers allows us to bridge the gap between your entity formation and its financial setup. Consult with Encor Group for Corporate Banking Assistance to secure your global financial infrastructure today. We’re committed to facilitating your international success with professional depth and efficiency.

Frequently Asked Questions

What is the primary difference between offshore and onshore banking?

The primary difference lies in the jurisdiction where the financial institution is located relative to your business’s primary place of registration. Onshore banking occurs within your domestic borders, while offshore banking involves facilities in international financial centers. These international hubs often provide superior multi-currency capabilities and access to sophisticated investment products that domestic retail banks don’t offer.

Is it legal for a business to hold an offshore banking account?

It is entirely legal for a business to maintain offshore banking accounts provided they comply with all international tax reporting standards. Transparency is now the global norm. You must fulfill all disclosure obligations, such as the U.S. FBAR requirement if your aggregate account value exceeds $10,000 at any point during the year. Legitimate businesses use these accounts to facilitate global trade and manage currency risk.

Which jurisdictions are considered the most stable for offshore banking in 2026?

Hong Kong, the United Arab Emirates, and Singapore remain the most stable hubs due to their robust regulatory frameworks and political neutrality. Switzerland also continues to show growth, with assets under management reaching CHF 9,284.0 billion in 2024. These jurisdictions prioritize institutional stability and provide the legal predictability necessary for complex corporate finance operations.

What documents are typically required to open a corporate offshore account?

Banks require a comprehensive set of corporate documents, including your Certificate of Incorporation, Articles of Association, and a detailed Register of Directors and Beneficial Owners. You must also provide a business profile that outlines your expected transaction volumes and primary counterparties. All documents generally require professional certification or an apostille to meet the bank’s underwriting standards.

How long does the offshore bank account opening process usually take?

The process typically requires between 4 and 12 weeks to complete. This timeline accounts for the rigorous due diligence and KYC protocols that institutional banks must perform. While digital banks or Electronic Money Institutions might offer faster onboarding, tier-one banks in premier jurisdictions conduct a more exhaustive review of your corporate hierarchy and source of wealth.

Can I open an offshore bank account without visiting the country in person?

Remote account opening is standard practice in 2026 for many offshore banking accounts. Professional intermediaries often facilitate this process through digital verification or by utilizing certified copies of your identification. While some traditional institutions in specific jurisdictions might still request a physical meeting, most global hubs have modernized their onboarding to allow for fully remote applications.

What are the minimum deposit requirements for international corporate accounts?

Minimum requirements vary significantly based on the institution and the jurisdiction. Digital platforms may require as little as $1,000, while established institutional banks often mandate initial deposits of $100,000 or more. You should also be prepared for ongoing balance requirements that ensure your account remains in good standing and eligible for preferred fee structures.

How does the Common Reporting Standard (CRS) affect my offshore account?

CRS facilitates the automatic exchange of your financial information between the bank’s jurisdiction and your country of tax residency. It means your account balances and interest income are reported to your local tax authorities annually. This system ensures total transparency and makes it vital that your corporate structure is fully compliant with all local and international tax laws.